Chargebacks are a growing—and expensive—problem for ecommerce companies. They’re not slowing down, either. Industry data shows disputes have surged over the last few years as “first-party misuse” (friendly fraud) becomes easier through banking apps and one-click dispute flows.

Statistics also show 40% of consumers who file chargebacks will do so again within 60 days—and half of those will repeat within 90 days. Once a customer learns the dispute path, they’re more likely to reuse it.

Banks and card networks make it simple for cardholders to contest a charge. Merchants end up paying the price—through lost revenue, inventory, shipping, fees, and operational time.

If you run an online store, you’ve probably dealt with this already. It’s frustrating: a customer orders, you fulfill, funds settle—and then the transaction gets reversed.

Often you don’t learn about the dispute until after it’s filed. So what now? Why are you “punished” for fulfilling an order? And how far should you go to prevent it from happening again?

Chargebacks come up constantly in our consulting work. Many teams aren’t sure how to respond or prevent them. This guide shows you how to act immediately when a chargeback lands—and how to reduce your dispute rate long-term.

First, we’ll cover what to do the moment a chargeback is filed. Then we’ll show prevention tactics that actually move the needle. Use these to minimize losses and keep your dispute ratio below card-brand thresholds.

Here’s what matters.

Don’t dispute every chargeback—triage fast

Most teams instinctively hit “dispute.” But card networks optimize the process for consumers, not merchants. You’ll win some, but indiscriminately fighting every case wastes time and fees.

Use a simple triage framework instead:

- Identify the reason code. Categorize as true fraud (stolen card), not as described/defective, canceled/returned, duplicate, subscription canceled, or “no recognition.” Each requires different evidence.

- Decide: accept or represent. Accept low-value, low-win-probability disputes to save fees and labor. Represent high-value cases, clear first-party misuse, or orders with strong proof (delivery, usage, policy acceptance).

- Assemble compelling evidence. Order/transaction details, AVS/CVV results, 3-D Secure/step-up authentication data, IP/device fingerprint, prior logins, communications, refund/return policy copy and acceptance, shipment scans and delivery confirmation, photos/signature for high-value goods, download/use logs for digital goods, and any prior refunds or replacements offered.

- Submit quickly via your processor’s portal. Templates and checklists reduce errors. Deadlines are strict—missing one means an automatic loss.

Smart triage keeps your team focused where wins are realistic, while you invest most energy in prevention.

Many merchants dispute cases they believe are illegitimate—often “friendly fraud,” when a cardholder bypasses the merchant and goes straight to the bank for a refund. You’ll win some of these if your evidence is airtight, but banks frequently side with the cardholder if your records are incomplete.

Bottom line: don’t waste cycles on no-hope cases. Fight selectively and invest the saved time into prevention tactics below.

Ship on time—and set accurate delivery expectations

Late or missing deliveries are a top trigger for chargebacks. Sometimes the package was late; other times it was delivered but unrecognized, misdelivered, or stolen (porch piracy). If a buyer files first and asks questions later, you lose either way.

- Publish honest ETAs at checkout and on PDPs. Two-day shipping is the default expectation in many categories; next-day and same-day are growing. Don’t promise speed your ops can’t hit.

- Provide real-time tracking immediately after fulfillment. Send the tracking link by email and SMS; include it on an order-status page the customer can access without logging in.

- Proactive delay alerts. Weather, carrier issues, and backorders happen. Email/SMS buyers as soon as you know—offer options: wait, switch item, partial ship, or refund.

- Proof of delivery for high-value orders. Require adult signature, capture delivery photos where available, and insure expensive shipments.

- Offer delivery alternatives. Carrier lockers, in-store pickup, and hold-at-location options reduce theft and “item not received” claims.

Clear, proactive communication prevents “I thought it never shipped” disputes before they start.

Consumer expectations continue to tighten, not loosen. The safest approach is to under-promise and over-deliver, then notify customers immediately if anything changes.

Monitor transactions—and block fraud before authorization

Don’t assume every order is legitimate. Screen transactions and add friction only when the risk justifies it.

- Use layered signals: AVS and CVV checks, device fingerprinting, IP geolocation, velocity limits (email, address, BIN, device), and deny/allow lists. Flag mismatches and unusual patterns (overnight shipping to a new address, high quantity of the same SKU, multiple cards on one device).

- Step-up authentication with 3-D Secure 2 (3DS2). On risky orders, trigger issuer authentication to shift fraud liability and reduce true-fraud chargebacks—especially useful for EU/UK SCA compliance and high-risk segments.

- Require complete billing details (AVS). Partial addresses or missing ZIP codes are a red flag; enforce full entry and re-try logic.

- Manual review lanes. For borderline scores, hold and review with a SLA so you don’t delay good customers.

Fraud losses are significant when you count fees and ops time—many merchants now spend several dollars in costs for every dollar lost to fraud. Prevention at the gateway beats representment later.

Provide exceptional, easy-to-reach customer service

Plenty of chargebacks happen because customers don’t know how to reach you quickly—or they think a bank dispute is faster than your support.

- Offer multiple channels (live chat, email, SMS/WhatsApp, phone) with response-time targets visible on your Help page. Add chat to order-status pages.

- Self-service returns/exchanges portal. If it’s easier to dispute than return, people will dispute.

- Monitor social mentions and DMs; treat complaints as opportunities to resolve issues before they become disputes.

- Set a clear quality bar. Ensure product descriptions and photos match reality. Misrepresentation is a fast path to “not as described” chargebacks.

Make it obvious that a direct refund is faster and cleaner than going through the bank—and then honor that promise.

Send post-checkout notifications and follow-ups

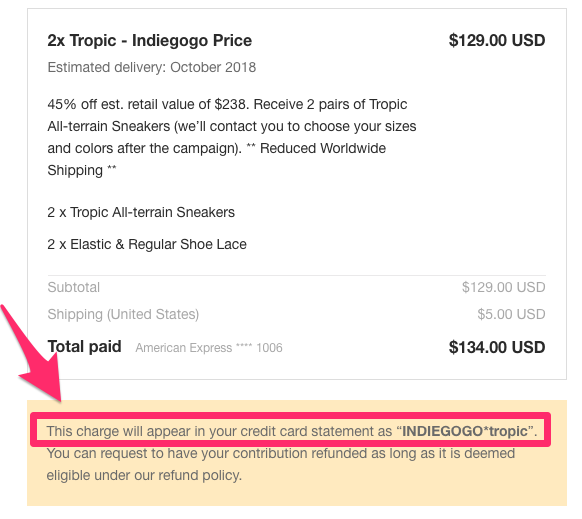

Immediately after purchase, tell customers how the charge will appear on their statement. If your storefront name differs from your legal billing descriptor, call that out to avoid “no recognition” disputes.

Explain exactly how the charge will read on their statement if the name of your ecommerce shop does not match your billing statement name. If customers don’t recognize the descriptor, they may file a chargeback without realizing it was your company.

It’s easy to avoid confusion by being transparent. Take a look at this confirmation email from Tropicfeel:

- Always send order confirmations with items, totals, taxes, shipping method, ETA, descriptor, and a prominent “Need help?” link.

- Send delivery confirmations and ask for quick feedback. If something’s wrong, invite the customer to reply or start a return—don’t make them hunt for support.

- For subscriptions/free trials: send pre-billing reminders, make cancellation one click, and confirm cancellations instantly via email.

These simple messages head off confusion and give customers an easy path to resolution with you—not their bank.

Choose a processor that supports you in disputes

How are you processing payments today? If support and tooling are weak, consider a gateway or PSP with strong dispute management.

- Look for tools like dispute portals with templates, evidence checklists, auto-population of order data, and reminders for deadlines.

- Enable issuer data-sharing programs (e.g., Visa Order Insight, Rapid Dispute Resolution; Mastercard Ethoca Alerts) to resolve complaints before they become chargebacks.

- Use 3DS2 selectively for risky orders to shift liability on true-fraud cases.

- Consider CE 3.0-style evidence for first-party misuse: login/device/IP history, prior undisputed transactions, and delivery/use records can make or break representment.

You’ll still lose some cases. But with the right processor, you’ll spend less time assembling evidence and more time preventing the next dispute.

Keep your dispute ratio below card-brand thresholds

Card networks monitor your dispute-to-sales ratio (and total dispute count) each month. If you exceed thresholds, you can be placed in a monitoring program with fines and additional scrutiny. As a rule of thumb, Visa often flags merchants around 0.9%+ dispute ratio with at least 100 disputes in a month, and Mastercard commonly flags merchants around 1.5%+ with 100+ disputes. Thresholds can vary by program and region—check your PSP’s latest guidance.

- Track your ratios weekly at the MID level; don’t wait for month-end surprises.

- Segment by source (marketing channel, product line, carrier, BIN, device, geography) to find the drivers and fix them.

- Create an “early warning” playbook for months when disputes spike (e.g., inventory delays, a defective batch, promo abuse).

Policy & UX fixes that reduce chargebacks long-term

- Make refunds easier than disputes. Prominent “Start a return” links, instant RMAs, and reasonable restocking rules reduce “go to bank” behavior.

- Use clear billing descriptors. Consider dynamic descriptors that include your brand + short product/category to improve statement recognition.

- Tighten product pages. Accurate titles, specs, sizing charts, comparison tables, and unedited customer photos lower “not as described” claims.

- Confirm order edits. When customers change addresses, sizes, or quantities, send a confirmation email/SMS that summarizes the change.

- Guard subscriptions. Transparent pricing, renewal dates at checkout, trial length in bold, and reminders before rebill. One-click cancel.

- Digital goods. Log successful logins/downloads, IP/device, timestamps, and in-app usage.

- High-value items. Signature on delivery, photo proof, tamper-evident packaging, and serial-number capture.

When it’s worth disputing a chargeback

- High-value orders with strong proof of delivery or digital use.

- Subscription misuse where you can show prior undisputed charges, clear disclosures, reminder emails, and successful login history.

- “No recognition” cases where your receipts and descriptor communications are clear and timely.

For small dollar amounts, it’s often cheaper to refund and blacklist abusers than to pay dispute fees and labor. For large, winnable cases, represent—and use the outcome to improve your prevention playbooks.

Conclusion

Chargebacks are a fact of ecommerce—but your response determines the cost. Don’t default to fighting everything. Triage quickly, represent only when the evidence is strong, and invest most of your effort in prevention.

Ship on time and communicate proactively. Give customers fast, omnichannel support and a simpler path to refunds than the bank. Screen orders with layered fraud tools, use 3-D Secure 2 when risk warrants it, and keep your dispute ratio below card-brand thresholds by tracking drivers weekly.

Send clear post-checkout messages that explain descriptors, deliver order and delivery confirmations, and follow up to catch issues early. Choose a processor with strong dispute tooling and issuer-data programs so you can resolve complaints before they become chargebacks.

Follow these steps and your store will spend less time chasing disputes—and more time serving customers and growing revenue.